Stablecoins vs CBDCs: Digital Money Explained

The global financial system is undergoing a historic transformation. As blockchain infrastructure matures and digital payments dominate everyday transactions, a new monetary framework is emerging. At the center of this shift lies the debate around stablecoins vs CBDCs, alongside the rise of tokenized deposits.

Over 105 countries representing more than 95% of global GDP are actively exploring Central Bank Digital Currencies (CBDCs). At the same time, stablecoins power billions of dollars in daily transactions across decentralized finance (DeFi). Meanwhile, commercial banks are experimenting with tokenized deposits to bridge traditional banking and blockchain networks.

This is not a competition of replacements. It is a convergence of digital money.

What Are CBDCs?

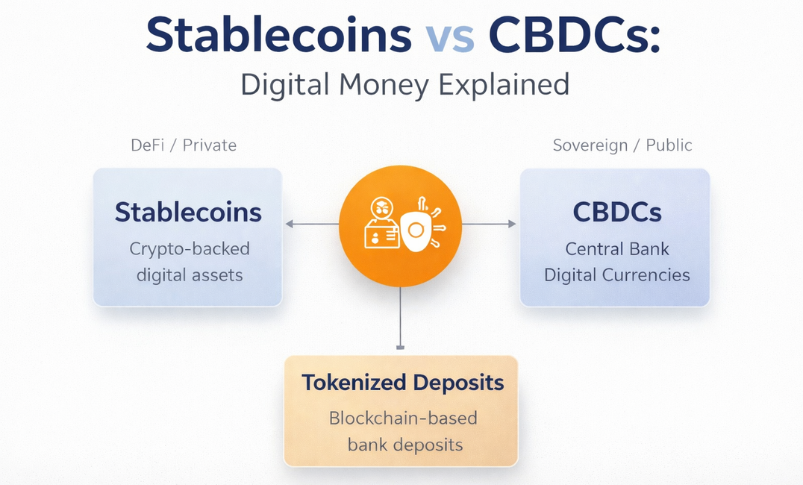

A Central Bank Digital Currency (CBDC) is a digital version of a sovereign fiat currency issued directly by a country’s central bank. Unlike cryptocurrencies or private stablecoins, CBDCs represent a direct liability of the central bank, similar to physical cash or reserves.

Governments are exploring CBDCs for several reasons:

- Declining use of physical cash

- Rising influence of private digital currencies

- Improving financial inclusion

- Enabling programmable monetary policy

- Increasing efficiency in cross-border payments

CBDCs are designed to modernize national payment systems while maintaining sovereign control over money issuance.

What Are Stablecoins?

Stablecoins are blockchain-based digital assets that are pegged to a fiat currency, commodity, or algorithmic mechanism to maintain price stability.

Unlike CBDCs, stablecoins are issued by private entities. They generally fall into three categories:

- Fully collateralized (1:1 backed by reserves)

- Crypto-collateralized

- Algorithmic stablecoins

Stablecoins are foundational to DeFi ecosystems. They enable:

- On-chain trading

- Liquidity pools

- Lending and borrowing

- Cross-border transactions

- Settlement without intermediaries

They combine the stability of fiat with the programmability of blockchain.

What Are Tokenized Deposits?

Tokenized deposits are commercial bank deposits issued in digital token form on blockchain networks. Unlike stablecoins, they remain within the regulated banking system and represent claims on commercial banks.

They provide:

- Faster settlement

- Blockchain interoperability

- Regulatory clarity

- Integration with existing banking systems

Tokenized deposits act as a bridge between traditional finance and decentralized infrastructure.

Stablecoins vs CBDCs: Key Differences

Understanding the difference between stablecoins and CBDCs is essential for evaluating the future of digital money.

Issuer

Stablecoins are issued by private companies.

CBDCs are issued by central banks.

Liability

Stablecoins represent a claim on a private entity.

CBDCs represent a direct claim on the central bank.

Regulation

Stablecoins operate under evolving regulatory frameworks.

CBDCs are sovereign instruments.

Use Case

Stablecoins dominate DeFi and global liquidity markets.

CBDCs focus on national payment systems and monetary policy.

The discussion around stablecoins vs CBDCs is less about competition and more about coexistence.

Why This Matters for Banks

Banks play two fundamental roles in the financial system:

- Credit creation

- Acting as intermediaries for payments

CBDCs could impact both.

If individuals shift deposits into CBDC wallets, banks may face reduced deposit balances. This could increase funding costs or pressure liquidity during financial stress.

However, most central banks favor a two-tier or intermediated model. In this structure, commercial banks provide wallets and customer-facing services while the central bank issues the digital currency. This approach minimizes disruption while preserving financial stability.

At the same time, payment revenues may decline as CBDCs introduce alternative settlement rails.

Design Choices That Will Shape the Outcome

The impact of CBDCs depends heavily on policy design decisions:

- Will CBDCs bear interest?

- Will there be limits on wallet balances?

- Will access be direct or intermediated?

- Will programmable features be enabled?

A non-interest-bearing CBDC with holding limits is less likely to disrupt commercial banking. Conversely, an unrestricted, interest-bearing CBDC could significantly reshape deposit dynamics.

These design decisions will define the balance between innovation and stability.

The Role of Stablecoins in CBDC Readiness

Stablecoins provide a live testing environment for programmable money. For financial institutions, engaging with stablecoins offers:

- Real-world blockchain settlement experience

- Exposure to decentralized liquidity markets

- Understanding of tokenized asset infrastructure

- Insight into operational risks

By experimenting with stablecoins, banks and institutions can prepare for future CBDC integration.

The Rise of DeFi and Digital Assets

Decentralized finance has already demonstrated how digital money can function without traditional intermediaries.

Key innovations include:

- Collateralized lending protocols

- On-chain market making

- Liquidity pools

- Automated settlements

As regulation evolves globally, financial institutions must engage with digital assets strategically rather than reactively.

The convergence of stablecoins, tokenized deposits, and CBDCs signals a new financial architecture.

The Future of Digital Money

The debate around stablecoins vs CBDCs is ultimately about structure, not survival.

CBDCs will modernize sovereign currency.

Stablecoins will drive innovation in global liquidity and decentralized finance.

Tokenized deposits will integrate regulated banks into blockchain ecosystems.

Together, they represent layered digital money systems that will coexist and interact.

The institutions that experiment early, engage regulators, and adapt their business models will lead the next phase of financial evolution.

Digital money is no longer theoretical. The convergence has already begun.

Follow us on